Acadlore takes over the publication of CiS from 2024 Vol. 12, No. 1. The preceding volumes were published under a CC BY license by the previous owner, and displayed here as agreed between Acadlore and the previous owner. ✯ : This issue/volume is not published by Acadlore.

Sustainability of Fiscal Policy in Democracies and Autocracies

Abstract:

This paper tries to identify the fiscal sustainability record of democratically and autocratically governed countries by applying various performance indicators (payment defaults, national debt, foreign assets) and also to clarify what effect the characteristics of a regime have on consolidation and inter- temporal budgeting efforts in a country. Important economic, social and environmental challenges of the future cannot be addressed if long term financial viability is not preserved in a country. The study identifies two key findings: while in the past, democracies have clearly found it easier to preserve their solvency and to avoid government bankruptcy, a similar advantage can no longer be detected for democracies in terms of reducing national debt and foreign debts. Why democracies, in spite of their arrangements with a sensitivity for the public good and for due process, are finding it so difficult to avoid shifting their debts to future generations (to undertake cutback measures and to provide sufficient financial foresight) can in principle be interpreted as the other side of the coin, namely highly presence-oriented interests boosted even further through the short democracy-specific time horizon.

1. Introduction

Against the background of the current financial and economic crisis, doubts have clearly increased about the general superiority of countries with a democratic constitution versus autocratically governed countries, in terms of the sustainability of their national finances. Moreover, to preserve long-term solvency and to achieve a balanced inter- generational budget that represents a fundamental condition for sustainable development. This article is grounded in the assumption that important economic, social and environmental challenges of the future cannot be addressed, if long term financial viability is not preserved in a coun- try. The dramatic household situation in several countries on the European periphery (Greece, Italy, Ireland, Portugal, Belgium), as well as other democracies on the globe (Japan, Iceland, USA), raise the question of whether democratic societies may not have systematic deficits in the consolidation of their national finances [1]. In comparison, it seems to have been considerably easier in the past for at least some autocratically governed countries (Kuwait, Russia, Saudi Arabia, China) to keep their na- tional debt under control and to make financial provisions for the future. To what extent these cases can be generalized, what specific cause and effect relationships exist be- tween a country’s regime type and the development of its national finances, and what other economic and social fac- tors play an important role in this context in addition to the degree of democratic or autocratic development, is subject of a highly controversial debate in the literature (cf. [2], [3], [4], [5], [6]). In principle, it can be stated that a fiscal policy that is oriented towards the criteria of sustainability is not only extremely important for the stability and organizational capa- bility of a modern political system (prevention of government crises through insolvency), but that shifting financial burdens onto the shoulders of future generations should be prevented, also to ensure a development that is fair to all generations (preserving future financial freedom to act) [7].

The special importance of this task explains the focus of our following considerations which is directed towards answers to the following key questions:

• How democratic and autocratic regimes perform in terms of the sustainability of their national finances (measured by the avoidance of payment defaults, the reduction of their national debt and their foreigndebt and the altitude of foreignassets)?

• Does the degree of democratization or autocratization really play a significant role in the sustainability of a country’s national finances, or could it be that there are other factors involved which influence this to a much greaterdegree?

To answer these questions, we will first offer some fundamental discussions about the sustainable development of national finances (Section 2) and then provide some thoughts about the relationship between the regime type and sustainable fiscal policy from the aspect of various theoretical approaches (Section 3). After an operationalization of dependent variables (performance indicators for financial sustainability) and independent variables (regime type and other potential explanatory indicators), in the course of which we will also deal with specific data problems in comparing democracy with autocracy, we will provide a quantitative analysis in Sections 4 and 5 (description and explanation of performance results). For that purpose, the study will first of all use descriptive analytical methods (performance determination via a comparison of means). In a second step, the resulting findings will be expanded and deepened by means of multivariate regressions for the more than 130 countries included in the study (small states with less than three million inhabitants were excluded from the study), for the period from 1990 to 2008 [8]. Finally, the results will be summarized and evaluated in Section 6. By following this course, we want to offer a theoretical contribution towards a connection at the interface of regime type and the discourse of fiscal sustainability, as well as provid- ing evidence of existing empirical connections.

2. Sustainable Fiscal Policy

Under what conditions a country’s fiscal policy can be called sustainable? To answer that question, it is useful, first of all, to look at the general definition of sustainabil- ity provided by the Brundtland Commission in 1987. In the sense of intragenerational, as well as intergenerational jus- tice, it means “to meet the needs of the present generation without compromising the ability of future generations to meet their own needs” [9]. The extension of political re- sponsibility beyond the generations living today to include future generations ([10] p. 27; [11] p. 7) implies an orien- tation towards the principle of making provisions for risks, towards the principle of intergenerational justice (fair equal- ization of burdens between generations) and the continu- ous development of opportunities for future generations (cf. [12] p. 28; [13] p. 54). Latitudes must be created today in order to be able to solve future problems.

Translated into sustainable fiscal policy, this means first of all (aspect of risk management) that the present-day budget policy should be such that it can be continued on a sustainable basis without plunging the nation into a finan- cial squeeze (cf. [14] p. 463; [15] p. 807; [16] p. 667). To deal with the serious danger of a government losing its ability to meet its financial commitments (national insol- vency) [17], a weak but risk-reducing sustainability can be achieved mainly through preserving a society’s credit wor- thiness and its capacity to pay its debts [18].

For an intergenerationally just fiscal policy (principle of strong sustainability, cf. [19] p. 23), it is also necessary to ensure a just equalization between generations and to pre- vent the exploitation of future generations (cf. [20] p. 31; [19] p. 110). It can be implied that a government policy that finances a nation through indebtedness is shifting burdens onto the shoulders of future generations (cf. [21] p. 27; [22]), as long as it is not only adjusting temporary fluctua- tions due to the economy reacting to extraordinary burdens or times of emergency (such as wars, natural catastrophes, etc., cf. [23] p. 294; [24] p. 124; [25]) or corresponding to the Pay-as-you-use principle [26]. In particular, the fi- nancing of purely consumer-oriented expenditures can be viewed as problematic (cf. [19] p. 115). A shifting of bur- dens occurs when subsequent generations experience a direct loss of benefits due to higher taxes necessary to amortize debts and to finance the servicing of debts (cf. [27] p. 250; [20] p. 1). Moreover, an excessive national debt can reduce the dynamics of a country’s economic de- velopment (crowding out of credit-financed private invest- ments, cf. [16] p. 627) and trigger a negative spiral of inter- est debt [28]. It could also limit the leeway for future invest- ments (such as R&D expenditures), resulting in a smaller total capital stock that is passed on to future generations. However, in the opposite sense, to continue providing future generations with opportunities, their financial degrees of freedom and action must be preserved (cf. [29] p. 13) and expanded in the form of the most positive rate of sav- ings possible, by not only investing in the future, but also by forming the greatest possible financial reserves. These reserves are then available in the future to be able to solve important economic, social or environmental problems. Up to what degree it might be useful also to finance invest- ments for the future through indebtedness is a subject of great controversy (cf. [30] p. 173; [31]). The problem of in- tertemporal budgeting lies in determining the most appro- priate taxation rate for future revenues and expenditures ([32] p. 19). Thus, it is in particular the implicit indebted- ness of a country that follows primarily from future claims under the pension system (pensions of public servants) or the health system that is difficult to assess, since it de- pends to a major degree on future labour and social legis- lation and on economic development (cf. [24] p. 221; [33]).

To identify the various dimensions of fiscal sustainability (risk management, intergenerational indebtedness and savings rate) as completely as possible, and to better eval- uate the performance of countries, this study uses a total of four performance indicators [34]. Following a trend in pol- icy analysis, we are evaluating the performance of regimes with the help of policy outcome variables [35]. However, since not only democracies, but also autocracies are in- cluded in this study, we are incurring a double problem with data. Not only is access to data in autocracies far more dif- ficult (selection bias) [36], but there is also the danger that the data made available may have been systematically falsified. In interpreting data, these problems must always be taken into account, even when—as in this case—generally accepted data sources (World Bank, IMF) are evaluated. To increase the validity of results, we used only such data in our performance evaluation which were obtained without the influence of autocratic states. Thus, we evaluated how nations performed in view of their solvency (risk management), based on the frequency of actual payment defaults (national insolvencies in the past). Consideration of de- fault events (suspension of due payments by a state), even though the exact conditions of a default can vary from case to case (cf. [37]), are based on robust, often used and less controversial data (cf. [38]).

To enable us to identify the (long-term) development of a country’s indebtedness situation in the most differenti- ated form possible, it seemed useful to look not only at a country’s general national debt (in relation to its GDP) [39], but also at its foreign debt (as measured by the amount of the country’s loans with the IMF) [40]. It can be argued that this foreign debt, in contrast to the debt owed to domestic creditors, is particularly problematic for a state, since some important instruments for lowering it (especially inflationary measures) are not available.

Finally, the picture of a performance evaluation would not be complete without considering a country’s intergen- erational austerity measures in addition to its mere indebtedness. The accumulation of foreign assets (measured as a country’s currency reserves in relation to its GDP) can be regarded as an important indicator.

The performance indicators we used are partly cor- related with each other (see Table 1). However, in no case does the measure of association reach a value of more than r = 0.15*** [41]. Not surprisingly, a particu- larly close relationship exists between the indicators of na- tional debt and foreign debt. On the other hand, no par- ticularly strong relationship can be detected between na- tional debt and payment defaults. It becomes clear that no deterministic relationships exist in that case if we realize that Argentina—in spite of a national debt of “only” 64% of GDP in 2001/2002 had to declare national bankruptcy, while Japan with a national debt that by now amounts to almost 200% of GDP has so far been able to avoid such a step due to its high economic power and low foreign debt (cf. [21] p. 12). Yet accumulated foreign reserves very of- ten seem to go hand in hand with low national debt and a low probability of payment default.

Prevention of payment default (Source for payment defaults in a country [38]) | Low national debt (Source for national debt in relation to GDP [42] | Low foreign (Source for pro capita foreign debt through IMF loans [42]; own calculations) debt | High foreign assets (Source for currency reserves in relation to GDP [42]; own calculations) | |

Prevention of payment default | 1.00 | 0.09 *** | 0.12 *** | -0.04 ** |

Low national debt | 0.09 *** | 1.00 | 0.15 *** | -0.12 *** |

Low foreign debt | 0.12 *** | 0.15 *** | 1.00 | -0.03 |

High foreign assets | -0.04 ** | -0.12 *** | -0.03 | 1.00 |

3. Fiscal Sustainability and Regime Type

Before any statement can be made on a theoretical level about the connection between fiscal sustainability and the regime type, the latter must be defined more precisely in all its possible variations. When we speak of political regime types, we can think of a continuum (cf. [43]), with the ideal (stable and contained) democracy at one extreme and a perfectly autocratic (totalitarian) regime at the other ex- treme, and with a broad grey area of mixed types (defective democracies, electoral autocracies) in between.

However, based on the lean definition of a democracy by Dahl (public contestation and the right to participate), one could argue that a cardinal criterion of differentiation can be found between democracies and autocracies which relates to the existence or non-existence of contested elec- tions. Their existence, which is tied to the three conditions of “(1) ex ante uncertainty: the outcome of the election is not known before it takes place, (2) ex post irreversibility: the winner of the electoral contest actually takes office, (3) repeatability: elections that meet the first two criteria occur atregularandknownintervals”([44]p.69),changesthe logic—as the argument continues—of a political system in a fundamental way, since it has fundamental impact on the responsibility of the government, the citizens’ possibilities to participate, and political competition in general.

The special advantage of the very lean differentiation we have chosen between democracy and autocracy, which includes neither aspects of division of powers nor of civil rights, is that it takes into account central institutional and procedural characteristics of a regime, but does not include the policy dimension, and this is especially important for the following performance evaluation [45].

For measuring the regime type, we used the current data set (DD) by Cheibub, Gandhi and Vreeland [44], [46], “Democracy and Dictatorship”, since it is not only based on the above named criteria of differentiating between the regime types and offers a comprehensive data set in lon- gitudinal and cross-sectional comparison, but also pos- sesses a high degree of construct and content validity. To increase the robustness of the results of the regression we additionally used a data set presenting a combination of the popular democracy indices Freedom House and Polity [47].

What theoretical expectations can be formulated in view of the fiscal performance effect of the regime types, which—as will be shown below—are following different log- ics of function?

In principle, the following considerations are based on the so-called Churchill Thesis, which calls democracy the relatively best form of government (cf. [48] p. 7566). Par- allel to the strengths of democracy in its fundamental fields of competence, the input legitimacy (through free and fair elections), through granting citizens participation and con- sideration for the preference of today’s (voting) citizens (cf. [49] p. 474), can also be assumed to have advantages with regard to its fiscal sustainability performance (avoidance of financial crises, taking the interests of future generations into account, willingness to save).

Arguments supporting this can be derived first of all from considerations of institutional theory. In principle, we can assume that stable and predictable institutional ar- rangements would favour a sustainable policy development that depends on long-term stable framework conditions [50]. Following Padro I Miquel [51], it is precisely the autoc- racies that are characterized by significantly lower institutional stability in comparison with democratic societies. In contrast to those, many autocracies find it much more diffi- cult after a change of rulers to organize a smooth transition without fundamental upheavals. However, the resulting po- litical instabilities and ruptures could be a heavy burden to sustainable policy development and could promote indebtedness (cf. [23] p. 303). Even the uncertainty about the long-term continuity of an authoritarian regime alone can— according to Padro I Miquel’s theory—promote an ineffi- cient type of rule that focuses on short-term goals [51], which, when in doubt, can hardly afford to be concerned with fiscal sustainability. In contrast, the institutional frame- work conditions in the democracies, which are more stable in the long run, increase the confidence of investors in their readiness to repay obligations (high degree of confidence) which gives them easier access to the credit market ([52] p. 36; [3] p. 2; [53]). The more favourable credit conditions, with other things being equal, not only facilitate the repay- ment of debts but also most likely decrease the probability of national insolvencies.

Other arguments speaking for a fiscal policy advantage of democracies can be derived from a stakeholder-centred theoretical perspective. Thus, advocates of the Rational Choice approach by Bueno de Mesquita et al. [54], [55] assume that the possibility of gaining influence over po- litical decisions is always more broadly based in demo- cratic countries than in autocratically governed countries. Since as a rule, the electorate in democracies, in con- trast to that in autocracies, consists of all eligible voters, a government—to forge a winning coalition on which its rule can be based—must to a much greater degree sat- isfy the interests of large parts of the population. For autocratic rulers, who only have to consider the interests of a sometimes very small winning coalition, which can consist, for example, of important military figures, high party functionaries or economic elites, it is rational to provide mainly private goods (means exclusively preferred by specific population groups) while democratic governments must offer far more public goods with a high regard for so- ciety as a whole. The prevention of payment defaults, with the associated consequences for the whole society, can be especially regarded as such public goods [56].

However, for the goal of a sustainably generation- oriented fiscal policy, it is also vital to what extent the in- terest of future generations is being taken into consider- ation by the electorate, which even in democracies can- not consist of more than all the voters alive today. Based on a debate that goes back at least as far as Tocqueville [57], and is currently making a come-back namely about democracy forgetting the future [49,58] the question arises whether democratic countries are finding it especially diffi- cult to integrate the interest of future generations with their political decision-making processes just because their key concern is to cater mainly to the preferences and interests of the people living today [59]. Such a consideration of in- terest in democracies seems plausible especially when it can be assumed that this is connected with advantages for the majority of present generations [60]. With respect to public indebtedness, it can now be argued that in general, citizens in a democracy want to avoid this (cf. [5] p. 28), but that the urge is always there to follow a short-range strategy of maximizing expenditures [61], also due to a fis- cal illusion among the electorate [62]. Under certain cir- cumstances it is also possible in democracies, in spite of the risk of being punished by the voters, to push through spending cuts (cf. [63] p. 36) and thus to limit the shifting of burdens to future generations. The urge to maximize short-term spending decreases particularly when the con- sequences of excessive indebtedness, usually perceived only as diffuse future costs, become acutely manifest for the electorate, for example in the course of a financial cri- sis (cf. [5] p. 20). This may indeed present an impor- tant difference in comparison with autocratically governed states, which can continue with an indebtedness strategy even in such an event for as long as the advantage for the small winning coalition is not over-compensated by the de- liberately accepted disadvantages for the country’s overall economy [64].

If we then look more closely at the policy formation and decision-making processes that predominate in democra- cies, there could be a problem with regard to sustainable fiscal policy in spite of the potential advantages of a high free-market orientation that will be discussed below. That problem could lie in the short political time horizon that characterizes democracies. A democratic government’s constant focus on meeting acutely occurring challenges under the additional pressure of constantly looming elec- tion campaigns [65] not only makes long-term planning and decision-making processes more difficult [66], but also in- creases the danger of excessively weighting present-day interests and pushing the problem into the future [58,67], which in turn could have negative repercussions on indebt- edness performance (cf. [68] p. 59; [69]). An autocratic ruler, once firmly in the saddle, may find it easier to escape such a short-term-oriented policy development. Since he does not have to provide regular free elections, there is also no danger of an electoral business cycle. In democra- cies, governments are always exposed to distribute voting present before elections [70], which increases the risk of excessive leverage.

The same may apply to the influence of powerful dis- tribution coalitions which, following Olson’s argument [71], are of especially great importance in developed democ- racies. Their lobbying can, so the thinking goes further, make economical budgeting in the sense of fiscal sustain- ability more difficult (cf. [72] p. 5), unless the political decision-makers put a stop to their (usually consumptive and presence-oriented) spending wishes [73]. In particu- lar, these distribution coalitions can also act as powerful obstacles to necessary fiscal cost-cutting programs. Cor- responding studies on government fragmentation shows, that the higher the number of decision makers in demo- cratic governments are (number of parties in a coalition, number of ministers in the cabinet, number of interest groups in the cabinet) the more difficult cost-cutting pro- grams [74], [75]. Especially in enforcing such unpleasant and sometimes harsh reforms usually directed against the interests of a majority of currently voting citizens, demo- cratic regimes seem to have far more difficulties than au- tocratic regimes. On the one hand, this has to do with the fact that democratic governments cannot easily rule with- out facing resistance from the usually large number of insti- tutional power limiters and veto players (established pub- lic control mechanisms). On the other hand, autocracies with their means of repression have an instrument—rarely available in democracies—to enforce a restrictive cost- saving policy even against fundamental resistance among their own population.

However, these potential advantages of autocracies, which are highly controversial especially since there are fewer effective forces that can prevent reforms [76], are connected with considerable costs. Thus, the well- developed apparatus of repression and suppression which the autocracies must maintain because of their small input legitimization (reduced participation rights) to safeguard the stability of their regime, can cause serious financial burdens in addition to other problematic consequences [77]. The lack of public control mechanisms, which on the one hand (partially) increases the regime’s ability to act, can in time complicate sustainable fiscal policy. Even if we assume—in the sense of Olson’s Stationary Bandit The- sis [78]—that the expectation of a long rule in autocracies leads to a policy based on long-term goals, there will al- ways be the latent danger that the authoritarian rule will de- teriorate without effective control. The lack of institutional safety mechanisms and of political competition for leader- ship positions always means, at least in the long run, an inefficient policy prone to corruption and only benefitting a small group of potentates [79]. On the other hand, the pub- licly controlled processes of competition in democracies ensure their ability to learn and to correct errors [57], since troubles become known earlier (early warning system) and politicians are obligated through their accountability to the majority of citizens to handle public funds as prudently and transparently as possible (reduced probability of corrup- tion). Historically, the highly competition-oriented politics in a democracy, in combination with institutional provisions and control institutions, also represents a favourable foun- dation for a system of market economy in general, as well as for an open and functioning capital market in particular (cf. [80] p. 206).

If after an analysis of the individual theory strands, we carefully compare all the above mentioned arguments with each other, we find that in spite of some objections (distinc- tive fixation with the presence, low resistance to distribution coalitions, short-term political time horizons), there are more arguments for superior sustainability performance in democratic countries (strong concern for the public good, well-defined controls on government, high institutional sta- bility, greater ability to learn and to correct errors, strong orientation towards competition). Starting out from the theoretical considerations, two similar hypotheses can be pro- posed about the connection between regime type and fis- cal risk management or between regime type and intergenerational justice / providing intergenerational opportunities:

Hypothesis 1: Countries with a democratic constitution find it easier than their autocratic counterparts to avoid national payment defaults.

Hypothesis 2: Altogether, democracies find it easier to lower their national debt. A democratic type of regime has a particularly dampening effect on foreign debt and a positive effect on the accumulation of foreign assets.

However, in addition to the characteristics of regime type (measuredby the Democracy/Dictatorship Index and the data set of Hadenius and Teorell), other social, and in particular economic factors have an impact on a country’s fiscal sustainability performance (cf. [81]). To accurately identify the actual impact of the regime type component, it is therefore necessary to include these factors into the investigation.

First of all, we must refer to a country’s state of eco- nomic development (per capita GDP) as a central measurement. While a high level of economic development, just as a strong growth momentum, provides a country with substantial opportunities to generate income (higher tax revenues, etc.), Wagner’s Law (cf. [82]) states that an economically developed society also tends to have clearly higher state spending (provision of cost-intensive govern- ment services). So we also take into account public expenditure (% of GDP) and tax revenues (% of GDP). While the overall effect is a matter of debate, it is probably true that altogether, a positive trade balance in a country generates additional resources for serving debts. As another relevant economic factor in connection with a country’s indebted- ness situation, we also considered the development of the country’s inflation rate in our later investigation. Here, it can be argued that high currency devaluation in the sense of an inflationary tax can tend to lower state indebtedness (cf. [83] p. 295; [23] p. 305). The natural (energy-) resources available in a country and the interest level were also regarded as potential indicators. While on the one hand, a low interest level makes it easier to repay debts, but also is an incentive for additional new indebtedness, a country’s wealth of resources can open additional sources of govern- ment income, but the intensive debate about (autocratic) rentier states shows (cf. for example, [84]) that it can also promote action by the government that is particularly inef- ficient and subject to corruption. With regard to factors of social structure, the population size of a country was taken into account. It can be regarded as a measure of a coun- try’s international importance. Here, it has to be examined whether the size (and thus the international relevance) of a country may possibly act as a buffer that makes a credit crunch and thus a national insolvency less likely (too bigto fail). We also reviewed the effect of a society’s age dis- tribution as another factor of social culture. Theoretically, one could argue that in an ageing society (coupled with a low birth rate), the existence of powerful distribution coalitions among the older population groups [71], the interests of subsequent generations, which are difficult to organize, are systematically neglected ([85], fading intergenerational altruism), and a high senior population rate could—through increasing social expenditures—lead to pressure for higher spending (see [86] p. 175; [87]). As the last factor, we also lookedattheextentinwhichacountryisinvolvedinmilitary conflicts as an indicator of whether it is particularly prone to indebtedness. It is relatively easy to argue that military conflicts are generally connected with considerable government spending while they allow the revenue situation of the country to erode. Table 2 shows all explanatory factors included in the later regressionanalyses.

Explanatory factors | Description |

Regime type (Democracy/autocracy) | Democracy/Dictatorship Index. Source: [46]. |

Regime type | Hadenius and Teorell Data Set. Source: [47]. |

Per capita GDP | Per capita GDP: Source: [42]. |

Growth of GDP | Annual growth of GDP, in %. Source: [41]. |

Public expenditure | % of GDP. Source: [42]. |

Tax revenues | % of GDP. Source: [42]. |

Trade balance | Trade balance. Source: [42]. |

Inflation rate | Inflation rate. Source: [42]. |

Energy imports | Net energy imports (% of energy use). Source: [42]. |

Real interest rate | Lending interest rate adjusted for inflation as measured by the GDP deflator. Source: [42]. Population |

Population ages > 65 | Population ages 65 and above (% of total). Source: [42]. |

Military conflicts | Intensity of military conflicts. Source: [88]. |

4. Fiscal Sustainability in Comparison

If we compare mean values of democracies and autocra- cies (and all their subtypes) using the four performance in- dicators (their general statistics are shown in Table 3) [89], the first thing that becomes apparent is that democratically governed countries are clearly better off in terms of their solvency (see Table 4). So the probability of payment de- faults in democracies is clearly lower than that of their au- tocratic counterparts (democracies 0.15; autocracies 0.34; total average 0.22). The values expressing connections showed the same trend when we based them on simple correlation calculations between democracy and payment defaults (r = −0.22***).

Payment defaults | National debt | Foreign debt | Foreign assets | |

Maximum | 1.00 | 289.80 | 812.91 | 58.30 |

Minimum | 0.00 | 1.40 | 0.01 | 0.01 |

Mean | 0.22 | 59.93 | 14.62 | 6.58 |

Standard deviation | 0.43 | 38.54 | 41.82 | 3.13 |

Number of cases | 1377 | 748 | 2394 | 2132 |

Type of regime | Payment defaults | National debt | Foreign debt | Foreign assets |

Total (1990–2008) | 0.22 | 59.93 | 14.62 | 6.58 |

Democracy (1990–2008) | 0.15 | 55.47 | 16.41 | 4.71 |

Autocracy (1990–2008) | 0.34 | 69.15 | 12.49 | 9.33 |

Total (1990–1999) | 0.19 | 68.17 | 13.95 | 4.05 |

Democracy (1990–1999) | 0.13 | 59.96 | 12.76 | 3.06 |

Autocracy (1990–1999) | 0.26 | 77.79 | 15.23 | 5.37 |

Total (2000–2008) | 0.06 | 53.00 | 15.35 | 9.24 |

Democracy (2000–2008) | 0.06 | 52.87 | 20.00 | 6.31 |

Autocracy (2000–2008) | 0.07 | 53.48 | 09.09 | 14.02 |

While the top positions were mainly held by the democ- racies of the OECD world, there were also some exceptions to this rule among democratically governed coun- tries (such as Argentina), while some autocracies (Singapore, Saudi Arabia) showed good results. Particu- larly poor results concerning government payment defaults were shown by countries such as Russia, Iran, Myanmar and especially the autocracies on the African continent (such as Niger, Togo or Cameroon) and countries in Cen-tral and South America (for example Honduras, Nicaragua, Peru, Argentina, Brazil and Venezuela). The democracies also seem to show a slight advantage in the category of lowering national debt [90], but when we look at details, this advantage is noticeably smaller than in the category of avoiding acute payment defaults. So among the group of countries with the highest indebtedness (national debt of over 100% of GDP) are quite a few democratic industrial countries (such as Japan, Greece, Italy and Belgium). Therefore, the connection between democratic rule and national debt is also less pronounced at r= 0.14**.

When we look at the development of foreign debt or the accumulation of foreign assets, democratic countries are at a disadvantage. In those categories, the majority of democratically governed countries fared by no means as well as their autocratic counterparts. On the contrary, some economically emerging autocracies (China, Indone- sia, Russia) did particularly well in expanding their financial reserves. Not only the average foreign debt of democra- cies exceeded that of the autocracies (democracies 16.41; autocracies 12.49; total average 14.62), dictatorships also seem to have been more successful in the past in accumu- lating foreign assets (democracies 4.71; autocracies 9.33; total average 6.58). Accordingly, there are connections be- tween democracy and foreign debt (r = 0.04*) and between democracy and foreign assets (r =0.07***). It would therefore certainly be out of place to speak of a general su- periority of democracies across all dimensions of the study.

This impression is reinforced when we take, in addition to the full time period (1990–2008), a closer look into the sub-time periods 1990–1999 and 2000–2008 (see lower column of Table 4). While democracy advantage with regard to payment defaults and sovereign debt is much higher in the 1990s, we can see a decrease in the 2000s. Even more pronounced are the differences in foreign debt and foreign assets between the 1990s and the 2000s. While democracies had slightly less accumulated foreign debt than autocracies in the 1990s, the result revolved in the 2000s. And with regard to foreign assets autocracies obtain in the 2000s on average more than twice as much as democracies. So they build their lead significantly in relation to the1990s.

5. Regression Analyses

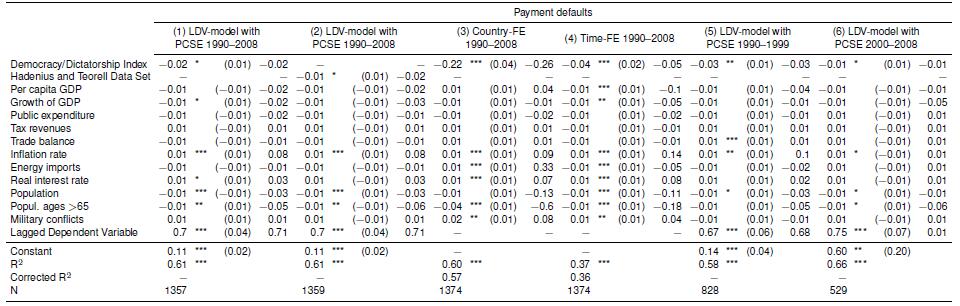

What picture, about the connection between type of regime and fiscal sustainability performance, emerges when we take additional potential explanation factors into account in the course of multivariate regression calculations? To be able to show results as robust as possible, we calculated a total of six models for each target dimension (see in detail Tables 5, 6, 7 and 8). Since the stationarity of the panel was checked for each target dimension, using the Levin- Lin-Chu-tests and/or a consideration of the scatter plots, we could dispense the use of dynamic models. So the first two models (each with a different regime type index) provide OLS regressions with a lagged dependent variable (LDV) and panel corrected standard errors (pairwise se- lection; PCSE). In doing so we can fix the problem of au- tocorrelation of the residuals (tested with the Wooldridge test). The included lagged dependent variable explains the relatively high corrected R2 of these models. See for the so called Beck/Katz-Standard [91]. To deal with the problem of heteroskedasticity (tested with the modi- fied Wald test) we also calculated country-fixed-effects and time-fixed-effects models (model 3 and 4). In doing so we can see coefficients ride of specific country or year ef- fects (for clarity reasons the results of the country and time dummy variables were not shown in the tables). Finally we added models for sub-period 1990–1999 and 2000– 2008 (OLS with LDV and PCSE) to see whether the differ- ences between them shown above have an influence. All explanatory variables for each model were taken into ac- count with a time variance of one year (T-1) to test their delayed impact in time on the dependent variable.

The results listed in Tables 5–8 basically confirm the findings which already show in the comparison of means, but they also draw attention to some other interesting con- nections.

Thus, the models concerning payment defaults (cf. Ta- ble 5), demonstrate a significant effect in favour of demo- cratically governed countries. This effect remains robust across all model specifications, thus confirming the previ- ous empirical results and theoretical assumptions. How- ever, it appears that the very strong positive effect of democracy, which is present in the 1990s, is weakening in the 2000s. While a low probability of default goes hand in hand with strong growth rate, government insolvencies co- incide with a high inflation and real interest rate and seem to occur somewhat less frequently in large and aged coun- tries. While in particular, the economic variables are thus exercising a marked influence on a country’s solvency, the factor of a country being prone to war is not reaching a significant explanation level across all models.

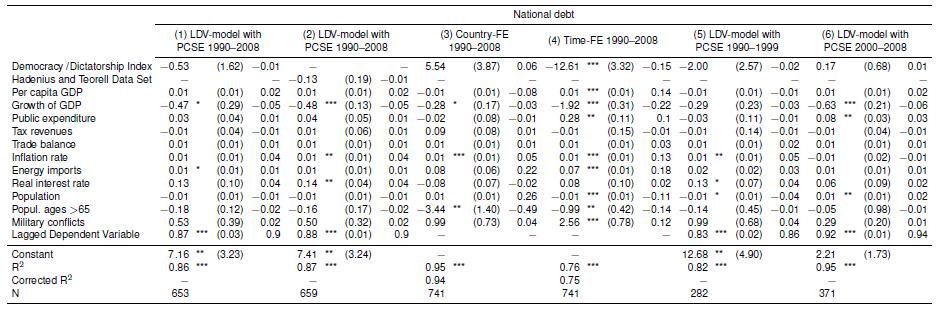

Low national debt in a country is closely connected with a high growth rate, while the level of economic develop- ment does not appear to have such an effect (cf. Table 6). The variable of regime type, which is at the centre of attention here, does show that democratically governed countries tend to lower their indebtedness more, but the difference lies in most of the models below the required significant range [92].

Looking at the different time periods, the debt dampening effect, which was in force in the 1990s in favor of the democracies, turns in the 2000s into its opposite (however without reaching a high level of significance).

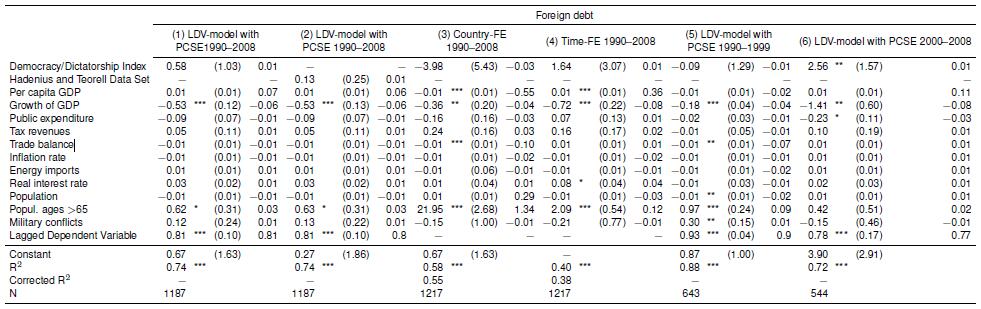

Definitely no advantage can be recognized for democracies when we look at foreign debt (see Table 7). Instead, the partial regression coefficient in this case shows a ten- dency towards higher foreign debts in democratic regimes (model 1, 2 and 4), although the difference does not reach a significant level. Considering the different time periods, it is striking that in the 1990s, foreign debt in democracies was less pronounced than in autocracies (however this relationship, controlling for the other factors, does not reach high level of significance). Yet, in the 2000s, democracies accumulated significantly more foreign debt than their autocratic opponents. So situation deteriorated for the democracies over time. While the foreign debt of a country with high economic growth rates and a positive trade bal- ance tends to be lower, aged societies seem to accumulate higher foreign debt.

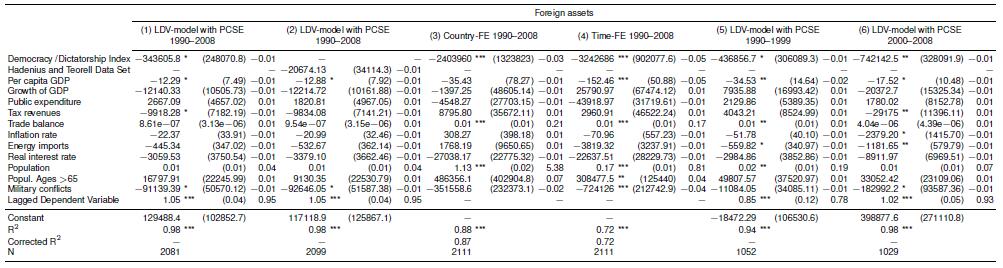

Looking at the last target dimension, the size of a country, as well as its low probability of involvement in war, seems to play an important role for the accumulation of foreign assets. Positive trade balance also seems to be helpful. By contrast, democratic governance represents a signified obstacle to the accumulation of foreign assets. This effect is robust and can be observed across all model specifications. Again, the situation for democracy deteriorated considering not the 1990s but the 2000s.

In total, it can be stated that under the effect of other indicators, the regime type shows a recognizable effect infavour of democratic countries only in terms of the avoid- ance of payment defaults. On the other hand, they seemto be less able than their autocratic counterparts to prevent the growth of foreign debts, not to mention their greater inability to form long-term financial reserves. Particularly problematic is also the fact that democracy tends to deteriorate its impact with regard to fiscal sustainability over the last two decades. Of course this result, which is somewhat sobering for the democracies, can be somewhat bright- enedwhenwetakeintoaccountthattheyarefarmoreded- icated than autocracies in taking financial action in futureoriented political areas. Thus, they are able to balance the burden they place upon future generations (through excessive indebtedness) with important future investments[93].

|

|

|

|

6. Conclusion

The objective of the study was to identify as closely as possible the financial sustainability performance of demo- cratic and autocratic regimes by looking at five target di- mensions. Financial sustainability is of fundamental im- portance because without it, important economic, social and environmental challenges of the future cannot be ad- dressed. The study generates two key findings. While in the past, democracies clearly had more success than their autocratic counterparts in preserving their solvency and in avoiding national bankruptcy, a similar advantage for democracies cannot be detected when it comes to the reduction of their national debt and their foreign debt and to the accumulation of foreign assets [95]. While reliable institutional framework conditions increase confidence in the creditability of democratically governed societies (creditors worry less about non-repayment), and evidently reduce the danger of government bankruptcy, no such con- nection seems to exist with regard to indebtedness performance. Why democracies, in spite of existing institutional and procedural arrangements sensitive to the public good (distinctive controls of government and ability to correct mistakes, large winning coalition) are having such a hard time in avoiding to shift burdens to future generations, to undertake cost saving efforts and to use adequate financial foresight, must basically be interpreted as the other side of the coin, namely a strong orientation towards present interests. This is promoted even more by the short time horizon typical for democracies. Overall, the associated incentives for indebtedness seems to be so powerful that they not only level out any potential differences with regard to regime type, but also that they remain in place even in the face of the potentially inefficient investment policy of autocracies which is so prone to corruption and has little future orientation.

The results presented here are based on data that ap- plied to the beginning of the current financial and economic crisis. For the time being, it remains to be seen to what extent they will remain robust beyond that time frame. Although the performance of democracies has tended to deteriorate in relation to autocracies over the 1990s and 2000s, past experience is giving us hope that in contrast to the autocratically governed countries, the democ- racies will have a greater repertoire of opportunities available to at least defend against the dangers of government bankruptcy. It remains to be seen to what extent this can be utilized in individual cases as well.

This calls attention to the need of further research which should extend from a more farreaching analysis of connections between regime type and fiscal sustainability on a theoretical level—especially to a more precise exploration of governance structures and causal mechanisms. In addition, it seems necessary to have a detailed look at the framework conditions of financial policy and at other potential explanatory variables (cultural factors, geograpical conditions, specific constellations of actors, etc.) for the policy performance analysis in this area of research that has not had much attention from the aspect of com- paring regimes.

The data used to support the findings of this study are available from the corresponding author upon request.

An older German version can be found under Wurster, S. Sparen Demokratien leichter?—Die Nachhaltigkeit der Finanzpolitik von Demokratien und Autokratien im Vergleich. dms-der moderne staat-Zeitschrift fü r Public Policy, Recht und Management. 2012; 5(2):269-290.

The authors declare that they have no conflicts of interest.